Buffing Out Volatility

You can hardly open your inbox these days without receiving an email about buffer exchange-traded funds. Also known as “defined outcome strategies,” buffer ETFs offer a way to hedge downside equity risk in exchange for lower participation during market upswings. There is typically a downside protection amount (the “buffer”), ranging from 10% to 100%, and a capped potential upside over a set period, typically one year.

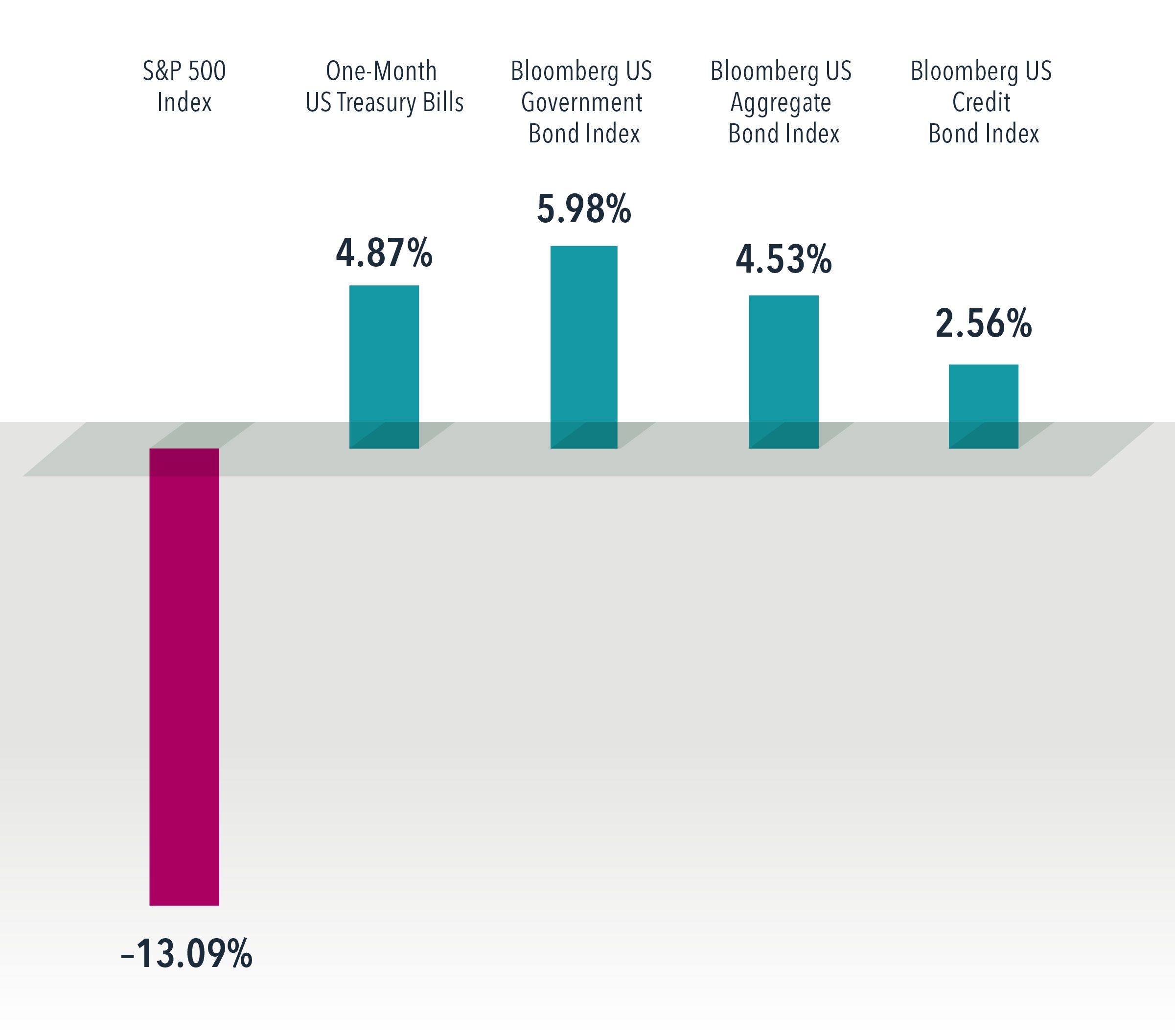

Softening the blow during equity market downturns is appealing for most investors. However, we already have a well-established asset category to help achieve this: fixed income. Historically, fixed income investments across a wide range of sectors have had a positive average return when equities have had a negative return. Since 1976, for example, the Bloomberg US Aggregate Bond Index had an average return of 4.53% in years when the S&P 500 Index had a negative return.

Some have questioned the diversifying benefit of fixed income based on recent episodes of rising correlations between stocks and bonds. It’s important to remember that shortterm past correlations do not predict future correlations, and historical data shows that the volatility reduction benefit has been insensitive to the correlation between stocks and bonds.

Investors who are worried about equity volatility can benefit from a fixed income allocation—and redirect unwanted buffer ETF emails to the junk mail folder.

Past performance is not a guarantee of future results.